There is a loud debate on whether allowing or limiting FDI in different sectors in India is in the nation's interest. What is surprising is that there is so little engagement with Indian direct investment abroad - FDI in reverse, so to speak.

At the end of FY 2011-12, the RBI estimated the accumulated stock of Indian direct investment abroad at $111.7 billion, over 50 per cent of the accumulated FDI stock in India of $219.6 billion. The stock of Indian direct investment abroad has grown over 11 times since the end of FY 2004-05! But even these staggering numbers do not reveal the full extent of outflows from India.

The stock of investment is built up through annual capital flows. The net outflow and inflow investment numbers of the RBI include a component termed 'reinvested earnings'. These refer to the portion of the profits from pre-existing investment in a country that has been reinvested as opposed to being paid out as dividend to the investor. Reinvested earnings do not affect the overall balance of payments (BOP) of a country, as they represent a movement of funds from the current account to the capital account rather than a cross-border flow.

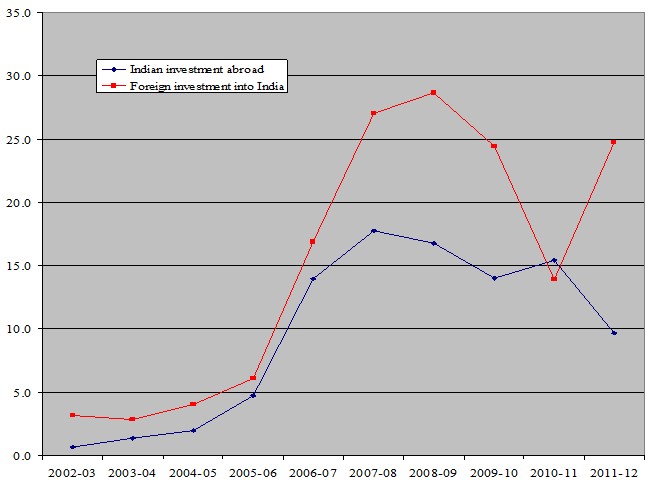

A comparison of the yearly flow of Indian direct investments abroad with FDI into India for the past decade, after excluding reinvested earnings from both flows, throws up some interesting facts.

Outflows moved more or less in tandem with FDI inflows from 2002-03 till 2009-10 and this raises the suspicion that they may be connected, at least partially! Further, from a balance-of-payments perspective, the net outflow in the last six years was nearly 65 per cent of the net inflow and in 2010-11, more direct investment actually went out of India than came into India!

The question that arises is that given the acute current account deficit and the scarcity of investment in several areas of the domestic economy, are such large outward capital flows in India's interest?

Who is investing abroad?

The bulk of investment abroad is investment by companies in the form of equity and loans into Joint Ventures (JV) and Wholly Owned Subsidiaries (WOS). Such investments amounted to about $70 billion in the five years till March 2012. In the five years till June 2012, just over 380 companies invested over $10 million each, accounting for over 82 per cent of the investments. Of these, grouping the companies by business conglomerates, the top 10 outward investor groups in the country were:

- Tata

- Bharti Airtel

- Essar

- Gammon

- Reliance

- Religare

- Suzlon

- Reliance ADAG

- Vedanta

- United Phosphorous

These investor groups, through their 35-odd companies, accounted for more than a third of the investment outflows during this period.

Companies also borrowed abroad to finance their foreign acquisitions against guarantees backed by Indian banks. The financial commitment in the form of guarantees by Indian companies in the last five years was to the tune of $61 billion, and this was over and above the $70 billion in equity and loans. Just five business groups - Tata, Bharti Airtel, Reliance, Reliance-ADAG, and Suzlon - accounted for over half of the total guarantees, pointing to the highly leveraged nature of their foreign acquisitions.

The net outflow in the last six years was nearly 65 per cent of the net inflow and in 2010-11, more direct investment actually went out of India than came into India! (click image to enlarge)

Suzlon accumulated huge debts during a global acquisition spree and is now in the news for defaulting on its foreign debt obligations amidst a slowdown in the global sales of its wind turbines. Most of its debt is owed to Indian public sector banks, and the company is reportedly being 'bailed out' by these banks, who will take an Rs.750 crores as losses on its account.

Where is the investment headed?

In order to determine whether outward investment by companies on such a scale is in the nation's interest, we need to know first where the investment is headed. Large scale acquisitions like the ones by Tata Steel, Tata Motors and Bharti Airtel are publicly known. However, surprisingly, the government is officially unaware of the actual destination of investments in many cases.

RBI regulations require companies investing in joint ventures and wholly owned subsidiaries to disclose the recipient of their investment. A perusal of RBI data reveals that these are mostly intermediaries, shell companies without operations. Few Indian companies directly invest in the entity that is the actual target of their investment.

There is a marked preference for locating these intermediaries in Singapore, Mauritius, and Netherlands - countries that provide an attractive 'tax neutral' regime for holding companies. These have been the top three investment destinations for Indian investors', together accounting for over 55 per cent of the outward investment in the period April 2008 to Feb 2012.

The distancing of the foreign target from the Indian investor is often through multiple layers of shell companies. Multi-tiered intermediate structures located across several countries are justified as necessary to exploit tax treaties between different countries to the most advantage. However these complex structures make it extremely hard to determine the actual destination and end use of investments.

The public interest in outward flows

The near absence of regulation of Indian direct investment flows abroad makes it open to abuse of various kinds. Some of the investment may well be channeled into areas prohibited by regulation, such as the acquisition of real estate. A part may be 'round tripped' back to India disguised as foreign investment, to hide the identity of the investor as well as to take advantage of tax concessions (offered to foreign investors from certain countries) and there is some circumstantial evidence for this.

Leaving abuses aside, what about investments genuinely made abroad?

Government policy makers, repeating textbook arguments, speak of the markets that will open up for Indian goods and services increasing exports and employment and the technology and skills infusion that will take place. Their concern, however, does not extend to evaluating if any of these benefits indeed accrue to the Indian economy, for even basic data on the end use of investments is not collected, leave alone metrics designed to measure benefits from capital export.

Another capital export project that is presented as being in the national interest is the acquisition of overseas energy assets - in coal, gas and oil by public sector and private companies, purportedly because these are steps towards achieving "energy security" for the country. Besides the public sector ONGC, business groups such as Adani, Essar, Reliance, Lanco and GMR have been acquiring large energy assets abroad.

Here again, the government has not cared to explain the costs and benefits to the country. How is public interest better served by the Adani or Lanco or GMR groups owning coal assets in Australia or Reliance acquiring shale gas assets in the US? The example of China is held up as an example to drum up support for the strategy of acquiring energy assets. If China, with its massive international reserves, has been actively acquiring energy assets abroad, there is also the example of Japan which has managed its energy requirements without acquiring any such assets.

It is far from clear if capital exports out of India are good for India. What is apparent, from the enthusiasm with which they have taken to it, is

that India's business conglomerates believe it is in their interest.